From frozen foods

to financial services

Diversifying revenue streams while strengthening existing customer relationships.

CHALLENGE

Model a new revenue stream with financial services products that address the unmet needs of existing food service customers.

OUTCOME

A financial security framework for evaluating and identifying ideal customers for financial support

A suite of three offerings, spanning the most common financial problems for restaurants

IMPACT

Gordon Food Service wanted to expand their business beyond traditional food distribution. Relish investigated other products and services restaurants heavily rely on and identified a gap in financial services. Current loan options offer predatory rates, take too long to come through, or don’t take the nuances of running a restaurant into account. Seeing an opportunity, we crafted a suite of loan products tailored specifically to the restaurant industry. These new offerings not only diversify the GFS revenue stream, but also provide a lifeline to the core customer—independent restaurant owners.

INTRODUCTION

Running a restaurant is no small task, with 60% failing within their first year. While capital doesn’t solve all problems, it can give restaurant owners enough time to figure things out and right the ship. Restaurants struggle to secure affordable funding, as they are deemed “high risk” by most lenders. If they are offered a loan, it is usually set at an exorbitant interest rate that places a heavy burden on them for years.

Relish set out to help GFS understand why, how, and when restaurants experience financial instability and need an influx of cash. We used this opportunity to step in and create a set of products that prioritizes the restaurant’s success over collecting loan interest. The long-term survival of a thriving, independent restaurant community provides stability to GFS, as well.

Research & Framework

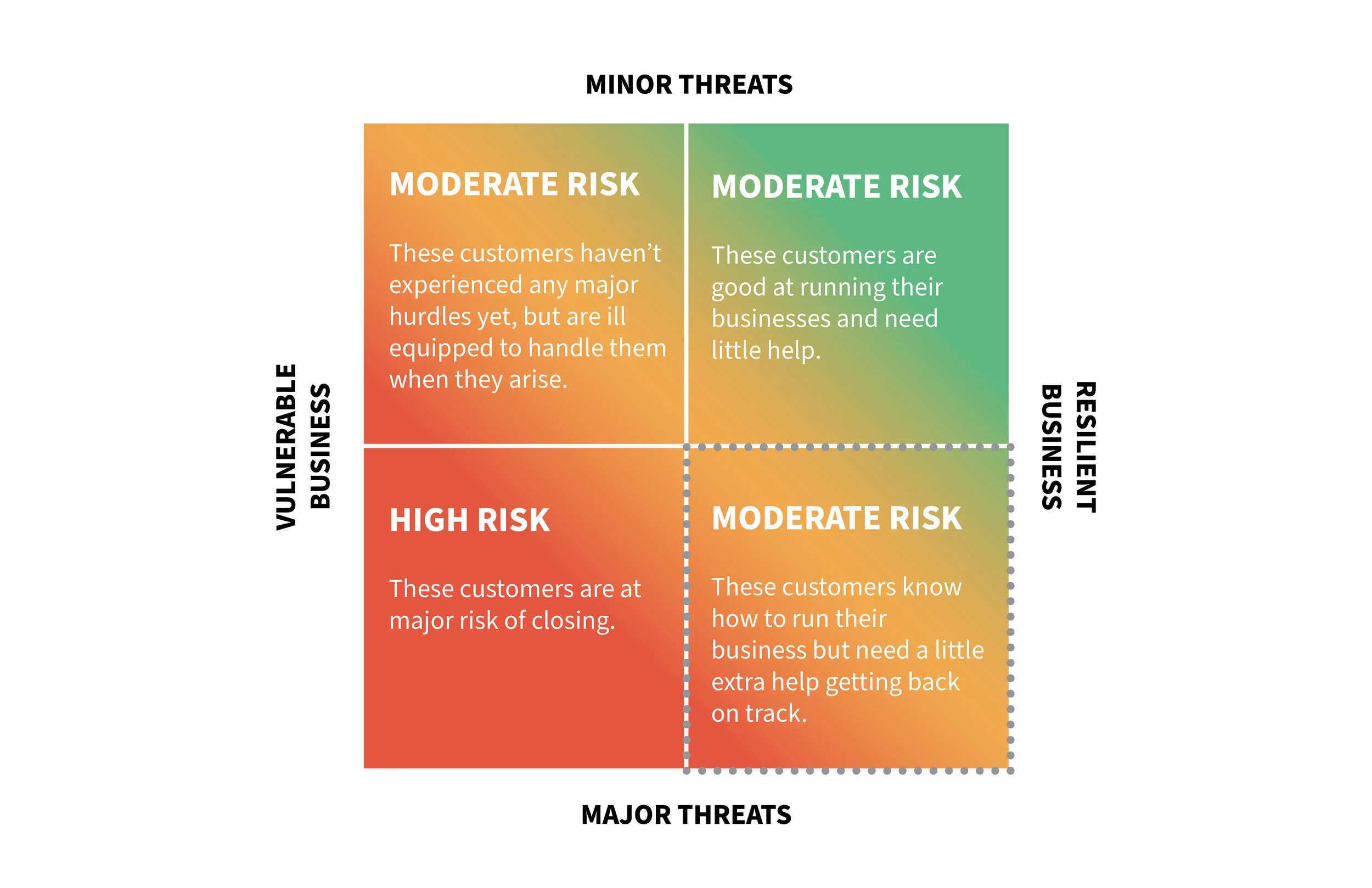

After speaking to a variety of restaurant operators, we decided to split financial risk measurements into internal and external factors.

The X axis measures the stability of a business, placing operators on a spectrum of how internally vulnerable they are based on the restaurant’s day-to-day operations. These aspects are a combination of practices within the restaurant’s control.

The Y axis measures the severity of external threats from the outside world. These threats are difficult to anticipate and are out of the restaurant’s control.

These two axes came together in a customer risk assessment framework. Our 2x2 mapped the operators, identifying what type of financial help is most often needed for each quadrant. We strategically decided to focus on the bottom right quadrant, with operators who run a stable business but face major external threats, as they are deliberate, analytical, and driven. They are most likely to pay back their loans on time and already have the know-how and drive to ensure that their business succeeds. With a little help from GFS at the right time, they can get their restaurant back on track.

Concepts

We believed microloans were the best entry point for our new product proposal, given the risk tolerance and level of funding needed to help bridge restaurants to success. Additionally, microloans also embody a spirit of assisting under-served or exploited populations with a reasonable interest rate, which resonates with our larger mission.

The concepts, Umbrella, Make it Work, and SOS, vary in the amount of money offered and the type of situation they are best suited for. After developing all three concepts, we made the strategic decision to focus on the first two, as SOS required a significant amount of money, manpower, and risk.

Rollout

Our go-to-market plan started with a pilot test with specific guardrails in place to limit the amount and type of customers these products were offered to. We needed the pilot test to help shape the final concepts, work out unforeseen issues, and answer key questions:

Who are the best people for this team?

How strongly will customers feel about switching business to GFS if offered these products?

What are the right channels to facilitate the process?

How does this business affect GFS?

We’d also track measurements for:

Customer business health before and after loan

Percentage of on time payments

Percentage increase in food spend for existing customers

Amount in food spend from non- GFS customers

Customer feedback throughout and overall satisfaction

In order to run the pilot to further evaluate and enhance our offering, we recognized the need to combine our restaurant knowledge with the experience of a financial services expert. The financial service expert would join our team to build out specifics around interest rates, payment plans and confirm our proposed business’ viability and profit model.

While it was not implemented at time of writing, this microloan resource is more important than ever, given the impact it could have had during the recently mandated restaurant dine-in closures as part of COVID-19. Looking ahead, there’s opportunity to expand into other quadrants with different financial products, restaurant best practices, or even consulting services. This is a unique way to help potential and long-time customers in a time of need, building loyalty with existing customers and ensuring they continue as a primary food distribution customer while still creating incremental revenue for GFS.